When it comes to managing personal or business finances, loans play a crucial role in helping individuals and organizations achieve their goals. Whether you’re planning to buy a home, start a business, or cover unexpected expenses, understanding the different types of loans available is essential. Choosing the right loan can save you money, reduce stress, and improve your financial stability in the long run.

In this comprehensive guide, we’ll explore the top types of loans you should know before applying, how they work, their pros and cons, and how to choose the best one for your needs.

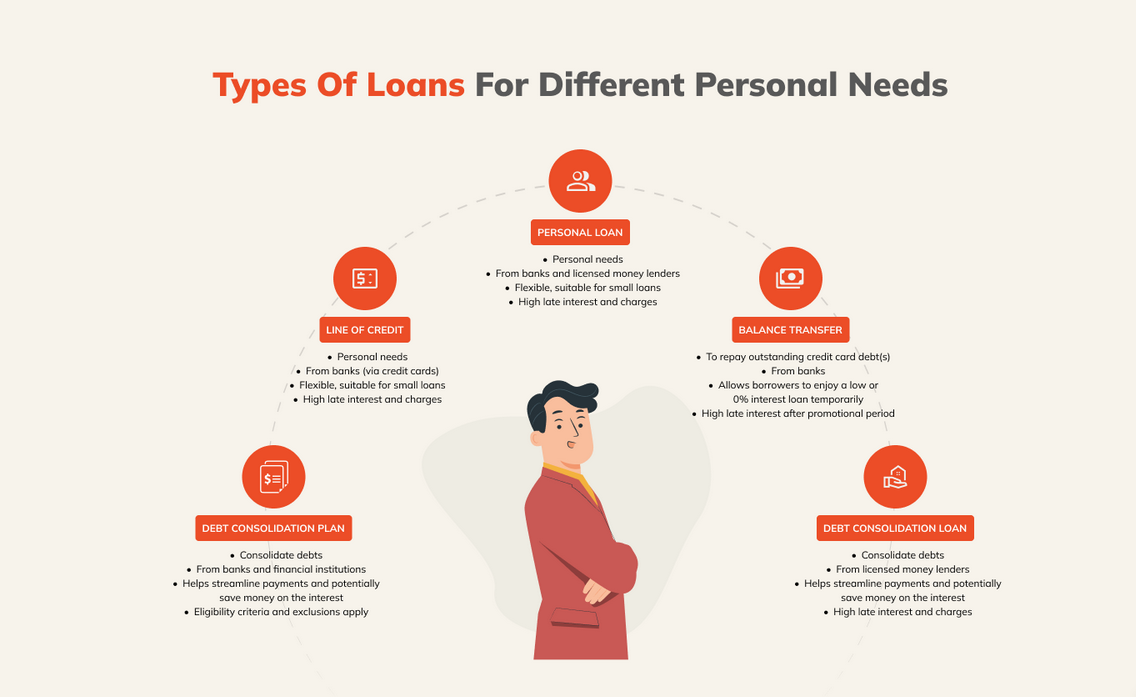

1. Personal Loans

Personal loans are one of the most common types of loans available. They are typically unsecured, meaning you don’t need to provide collateral such as a house or car.

Key Features:

- Fixed or variable interest rates

- Flexible use (medical bills, travel, debt consolidation, etc.)

- Repayment terms usually range from 1 to 5 years

Pros:

- No collateral required

- Fast approval process

- Flexible usage

Cons:

- Higher interest rates compared to secured loans

- Strict credit score requirements

Personal loans are ideal for individuals who need quick access to cash without risking their assets.

2. Home Loans (Mortgages)

Home loans, also known as mortgages, are used to purchase real estate. These are secured loans where the property itself acts as collateral.

Key Features:

- Long repayment periods (15–30 years)

- Lower interest rates compared to unsecured loans

- Fixed or adjustable interest options

Types of Home Loans:

- Fixed-rate mortgage

- Adjustable-rate mortgage (ARM)

- Government-backed loans

Pros:

- Lower interest rates

- Enables property ownership

- Tax benefits in some countries

Cons:

- Long-term commitment

- Risk of foreclosure if payments are missed

Home loans are essential for anyone looking to invest in property or buy a home.

3. Auto Loans

Auto loans are specifically designed for purchasing vehicles such as cars, motorcycles, or trucks. Like home loans, they are secured loans.

Key Features:

- Loan terms typically range from 3 to 7 years

- Fixed interest rates

- Vehicle serves as collateral

Pros:

- Easier approval compared to unsecured loans

- Competitive interest rates

- Helps build credit history

Cons:

- Depreciation of vehicle value

- Risk of repossession

Auto loans are ideal for individuals who want to own a vehicle but prefer to pay in installments.

4. Student Loans

Student loans are designed to help cover the cost of education, including tuition, books, and living expenses.

Key Features:

- Lower interest rates

- Flexible repayment options

- Deferred payments while studying

Types:

- Federal student loans

- Private student loans

Pros:

- Affordable repayment plans

- Grace period after graduation

- Investment in future earning potential

Cons:

- Long-term debt burden

- Interest accumulation over time

Student loans are a valuable tool for investing in education but require careful planning.

5. Business Loans

Business loans are designed to help entrepreneurs start, expand, or manage their businesses.

Key Features:

- Can be secured or unsecured

- Used for equipment, inventory, or operations

- Various loan sizes and terms

Types:

- Term loans

- Working capital loans

- Equipment financing

Pros:

- Supports business growth

- Flexible financing options

- Tax-deductible interest (in some cases)

Cons:

- Requires strong business plan

- Risk of financial loss

Business loans are essential for entrepreneurs looking to scale their operations.

6. Payday Loans

Payday loans are short-term, high-interest loans designed to cover urgent expenses until your next paycheck.

Key Features:

- Small loan amounts

- Short repayment period (usually 2–4 weeks)

- Minimal requirements

Pros:

- Fast approval

- Easy access

Cons:

- Extremely high interest rates

- Debt cycle risk

Payday loans should be used with caution and only in emergencies.

7. Credit Card Loans (Revolving Credit)

Credit cards offer a form of revolving credit, allowing users to borrow up to a certain limit.

Key Features:

- Flexible borrowing

- Minimum monthly payments

- High interest rates

Pros:

- Convenient

- Useful for short-term expenses

- Rewards and cashback options

Cons:

- High interest if not paid in full

- Easy to accumulate debt

Credit cards are useful but require disciplined usage to avoid financial problems.

8. Debt Consolidation Loans

Debt consolidation loans allow you to combine multiple debts into a single loan with one monthly payment.

Key Features:

- Simplifies repayment

- Often lower interest rates

- Fixed repayment schedule

Pros:

- Easier financial management

- Potential interest savings

- Reduced stress

Cons:

- May extend repayment period

- Requires good credit

This type of loan is ideal for individuals struggling with multiple debts.

9. Secured Loans

Secured loans require collateral, such as property, savings, or assets.

Key Features:

- Lower interest rates

- Higher borrowing limits

- Reduced risk for lenders

Pros:

- Easier approval

- Lower interest costs

Cons:

- Risk of losing collateral

- Longer approval process

Secured loans are suitable for large expenses where lower interest is important.

10. Unsecured Loans

Unsecured loans do not require collateral and are based on your creditworthiness.

Key Features:

- No asset risk

- Faster approval

- Higher interest rates

Pros:

- No collateral needed

- Quick access to funds

Cons:

- Higher interest rates

- Lower loan limits

These loans are best for borrowers with strong credit profiles.

11. Fixed-Rate Loans

Fixed-rate loans have a constant interest rate throughout the loan term.

Key Features:

- Predictable payments

- Stable interest rate

Pros:

- Easy budgeting

- Protection from rate increases

Cons:

- Higher initial rates compared to variable loans

Ideal for borrowers who prefer stability.

12. Variable-Rate Loans

Variable-rate loans have interest rates that can fluctuate over time.

Key Features:

- Rates tied to market conditions

- Payments may change

Pros:

- Lower initial rates

- Potential savings if rates decrease

Cons:

- Uncertainty in payments

- Risk of higher costs

Suitable for borrowers comfortable with financial risk.

How to Choose the Right Loan

Choosing the right loan depends on several factors:

1. Purpose of the Loan

Determine why you need the loan—whether for personal use, business, or investment.

2. Interest Rates

Compare rates from different lenders to find the most affordable option.

3. Repayment Terms

Choose a repayment period that fits your budget.

4. Fees and Charges

Look for hidden fees such as processing fees or penalties.

5. Credit Score

Your credit score affects eligibility and interest rates.

Common Mistakes to Avoid

- Borrowing more than you need

- Ignoring loan terms and conditions

- Choosing loans with high hidden fees

- Missing payments

- Not comparing lenders

Avoiding these mistakes can save you from financial stress.

Final Thoughts

Understanding the different types of loans is the first step toward making smart financial decisions. Each loan type serves a specific purpose and comes with its own advantages and risks. By carefully evaluating your needs, financial situation, and repayment ability, you can choose a loan that supports your goals without putting unnecessary strain on your finances.

Before applying for any loan, always compare options, read the fine print, and ensure you have a clear repayment plan. A well-chosen loan can be a powerful financial tool, while a poorly chosen one can lead to long-term challenges.